This section will be the most uncomfortable for many Americans to read. It contains no comfortable surprises. But knowing this before you move, rather than discovering it two years in -saves money, avoids penalties, and removes a lot of stress.

The United States is one of only two countries in the world (along with Eritrea) that taxes its citizens based on citizenship rather than residency. This means that even if you live full-time in Auckland, work for a New Zealand employer, and spend zero days in the US, you must still file a US federal tax return every year reporting your worldwide income. Moving to New Zealand does not change this.

This surprises many Americans who assume that once they leave, the IRS no longer has a claim on their income. It does.

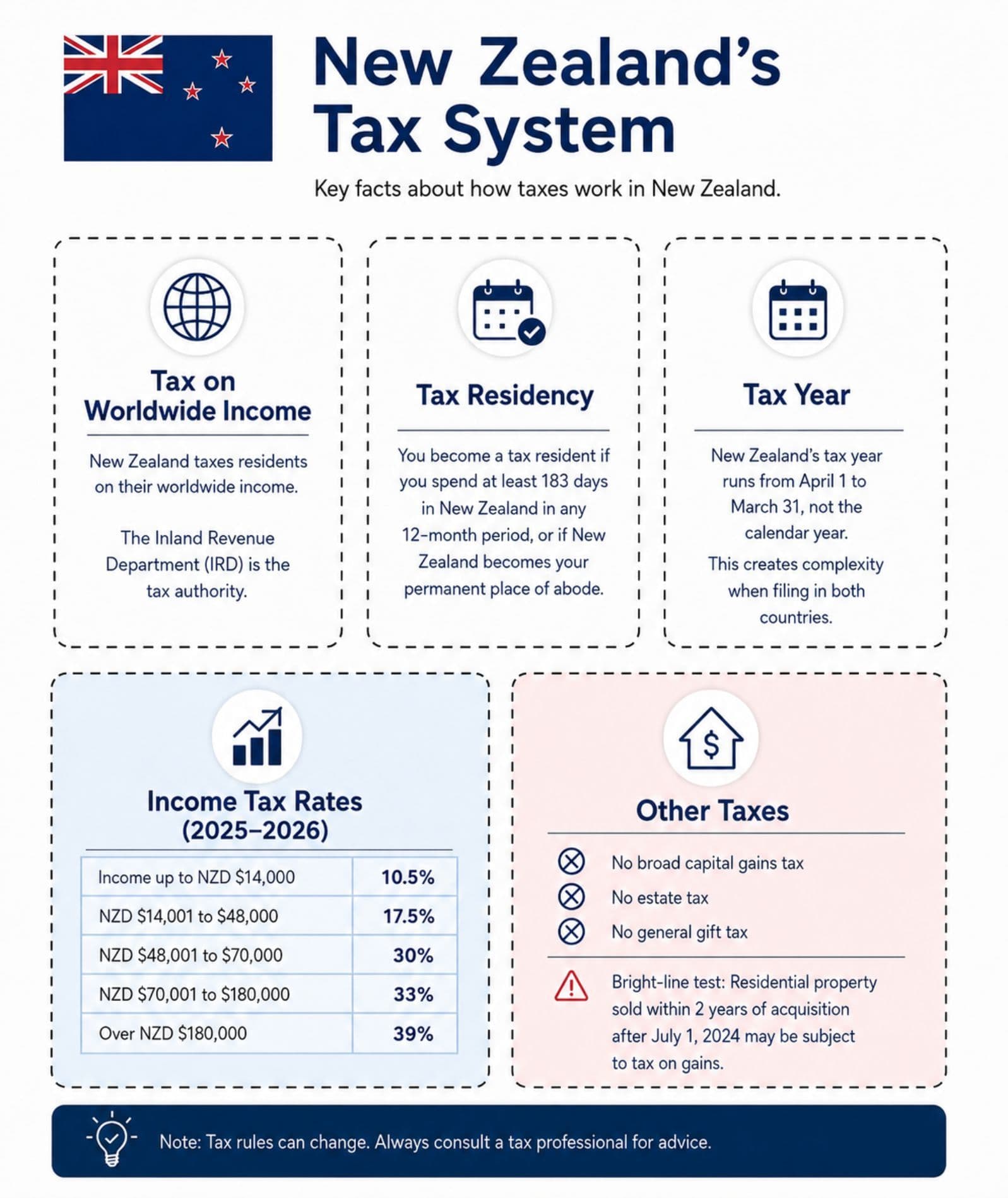

New Zealand taxes residents on worldwide income. New Zealand's Inland Revenue (IRD) is the tax authority. You become a New Zealand tax resident if you spend at least 183 days in the country within a 12-month period, or if New Zealand becomes your permanent place of abode.

New Zealand's tax year runs April 1 to March 31 not the calendar year. This creates coordination complexity when filing in both countries.

New Zealand income tax rates for individuals in the 2025–2026 year:

New Zealand has no broad capital gains tax, no estate tax, and no general gift tax. However, there is a bright-line test for residential property sold within 2 years of acquisition after July 1, 2024 may be subject to tax on gains.

The US and New Zealand have a tax treaty in place. The IRS maintains treaty documents here. The treaty establishes which country has primary taxing rights on different types of income employment income, pensions, dividends, interest, and royalties.

However, the treaty contains a saving clause that preserves the US right to tax its own citizens as if the treaty did not exist. This limits how useful the treaty is for ordinary American expats. It functions mainly as a backstop rather than a shield.

Two mechanisms help most Americans living in New Zealand reduce or eliminate double taxation:

Foreign Earned Income Exclusion (FEIE): Form 2555 lets you exclude up to $130,000 of foreign earned income from US taxation in 2025. To qualify, you must pass either the Physical Presence Test (330 days outside the US in a 12-month period) or the Bona Fide Residence Test (established residency in a foreign country for a full tax year). The FEIE covers earned income only wages and self-employment income. It does not cover investment income, rental income, or pension income.

Foreign Tax Credit (FTC): Form 1116 lets you claim a dollar-for-dollar credit on income taxes already paid to New Zealand. Because New Zealand's tax rates are often higher than US rates on equivalent income, the FTC frequently eliminates the US tax bill entirely for NZ residents.

Many US expats in New Zealand find the FTC more effective than the FEIE, particularly at higher income levels. Some use both but not on the same income.

If you open a New Zealand bank account and you will and the aggregate balance across all your foreign accounts exceeds $10,000 at any point during the year, you must file FinCEN Form 114 (FBAR) by April 15 (extendable to October 15). This includes checking accounts, savings accounts, KiwiSaver, and investment accounts.

Missing the FBAR filing triggers steep penalties up to $10,000 per violation for non-willful failures. This is not theoretical. The IRS enforces it.

The Foreign Account Tax Compliance Act requires foreign financial institutions to report US account holders to the IRS. New Zealand banks comply. ANZ, ASB, BNZ, Westpac, and Kiwibank all report US citizen account holders to the IRS automatically. You do not need to do anything to trigger this it happens regardless. What you need to do is make sure your own FBAR and Form 8938 filings match what the banks are reporting.

KiwiSaver is New Zealand's workplace retirement scheme. Employees contribute 3%, 4%, 6%, 8%, or 10% of their gross salary. Employers must contribute at least 3%. The government used to contribute NZD $521 per year; from July 2025 that was reduced to NZD $260.72 with an income cap of NZD $180,000.

The problem for Americans: the US does not treat KiwiSaver as a tax-deferred retirement account. The IRS may classify it as a foreign grantor trust or a passive foreign investment company (PFIC), triggering annual US tax on gains inside the account and requiring Forms 3520 and 3520-A. These forms carry large penalties when filed late even if no additional tax is owed.

Some Americans contribute only the minimum to keep the employer contribution, then halt further contributions. Others contribute more and manage the reporting. Both approaches are valid but the decision should be made with a US-qualified expat tax advisor, not in isolation.

The US and New Zealand do not have a Social Security Totalization Agreement. Multiple sources including the IRS confirm this. This means self-employed Americans in New Zealand can face US self-employment tax (15.3% on net earnings above the threshold) even while also paying New Zealand income tax and ACC levies. Employees working for a New Zealand employer are not subject to US FICA, but contractors and the self-employed face more complexity.

Hire a US expat tax specialist before you move not after. Not six months after you arrive and have already made decisions. Before. Firms like Taxes for Expats, Bright!Tax, H&R Block Expat, and Greenback Tax all specialise in this. Fees are $500 to $1,500 per year for straightforward returns. The cost of getting it wrong is far higher.

Need help with your application or background check?

Contact us now and speak with a dedicated Globeia expert today.